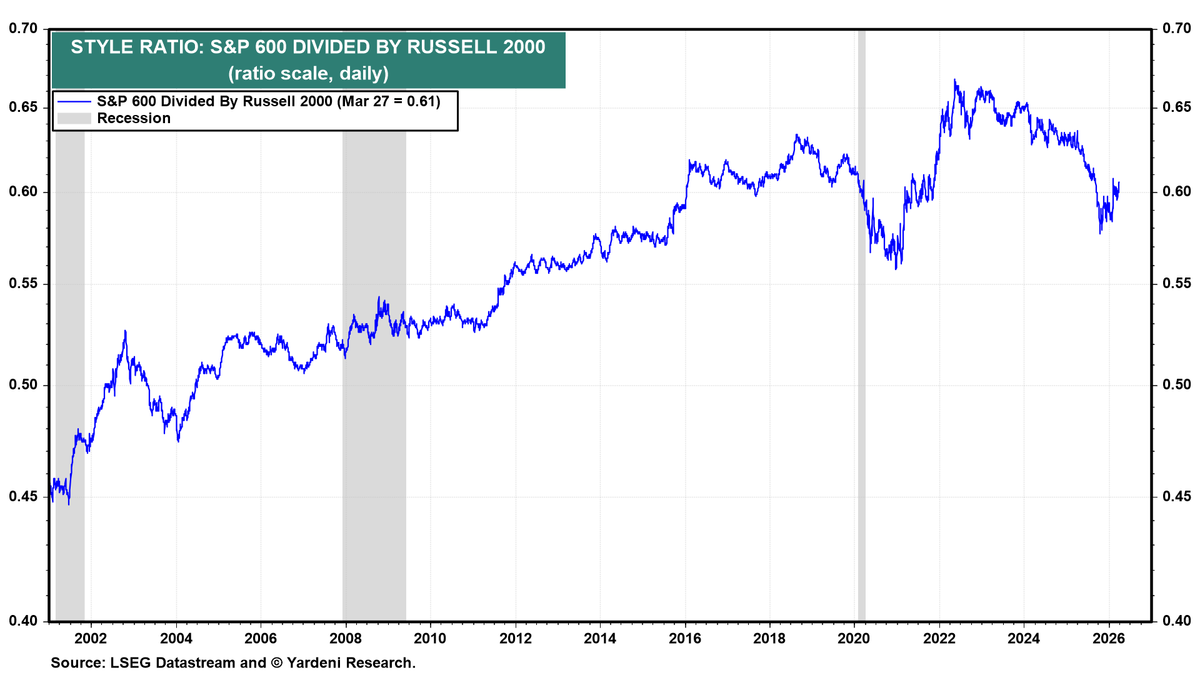

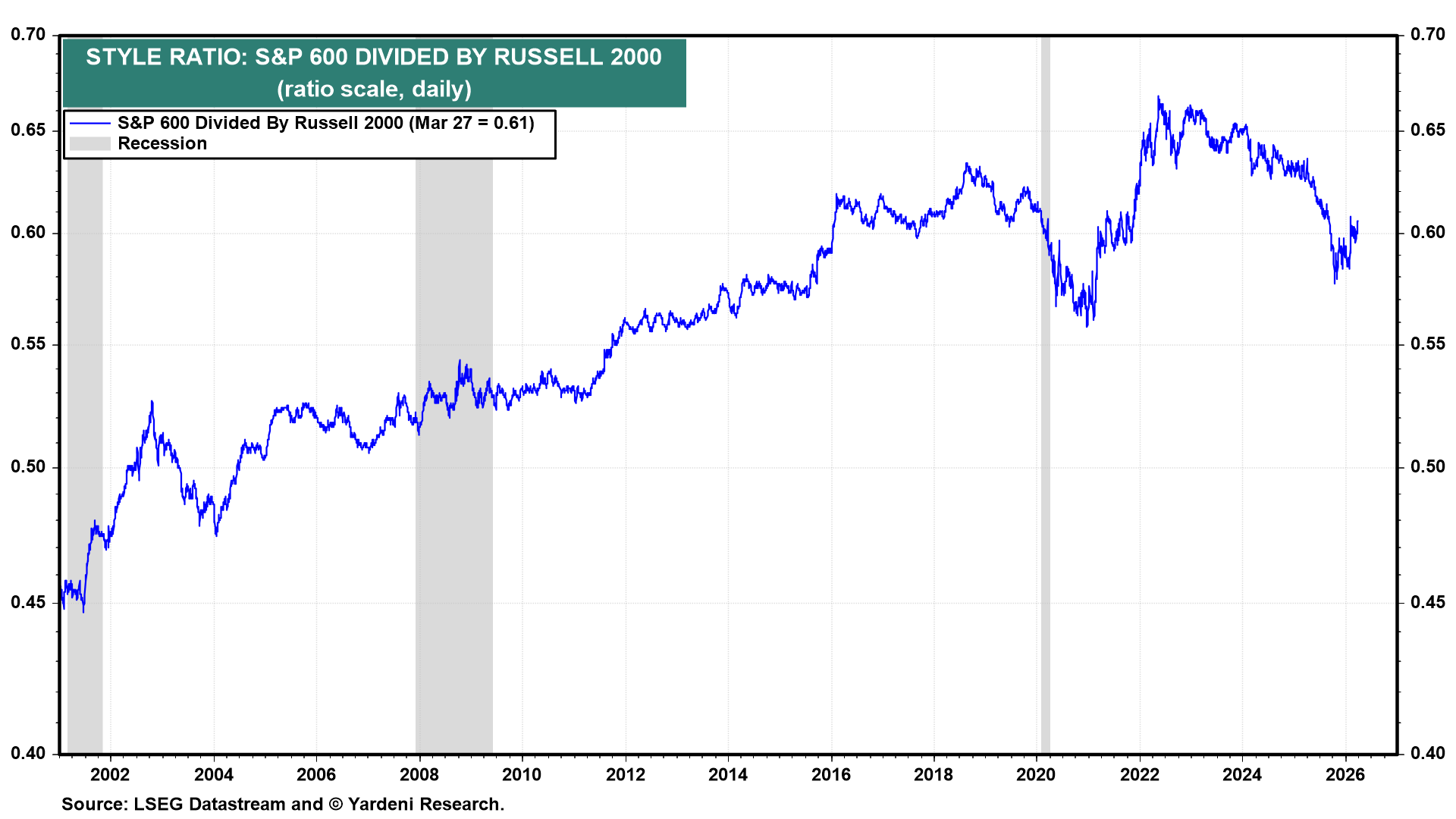

Small cap quality vs junk

Higher quality small caps outperform junk.

The long-term trend is quality outperforming junk inside small caps.

When this ratio:

- Falls → junk/speculative names outperform

- Rises → quality outperforms

The ratio rises from ~0.45 (early 2000s) → ~0.67 (2022 peak). That’s structural outperformance of S&P 600 vs Russell 2000

Why?

- S&P 600 requires profitability

- Russell 2000 includes a lot of junk / unprofitable names

👉 This is the Quality Minus Junk (QMJ) effect inside small caps

2020–2021 "Meme Stock" Bubble

2021 trough to ~0.55 was:

- Zero rates → speculative boom (2020–21)

- Then sharp tightening → junk collapse

👉 Classic “junk rally → junk crash → quality dominance” cycle

2023–2025 "A.I." Bubble

Ratio falls from ~0.66 → ~0.58

- Lower-quality names outperformed in speculative boom

- High-quality names outperformed since late 2025 junk collapse

👉 Another classic example of the “junk rally → junk crash → quality dominance” cycle

Today

We’re in a “risk-on / early-cycle” phase inside small caps

- When ratio is high (like 2022) → quality crowded → future returns compress

- When ratio falls (like now) → dispersion reopens → opportunity builds

Quality is relatively cheap again.

This chart is saying:

- Structural truth: Quality small caps beat junk over time

- Cyclical reality: Junk periodically outperforms during easing/liquidity phases

- Current setup: We’re in a quality rebound phase

👉 Which means, the next major move is likely continued quality leadership as macro tightens and earnings dispersion reasserts.